PerspectivesLatest

Moving beyond market episodes to build scenarios for asset allocation

We decompose market drivers over multiple years and outline how this helps define forward-looking scenarios

Read more

Stay up-to-date on our latest research and views on asset allocation topics:

We decompose market drivers over multiple years and outline how this helps define forward-looking scenarios

We revisit the widely used sum-of-parts model for expected equity returns using discounted cash flow logic

We discuss how the new market regimes and industry trends require increased granularity and scenario capabilities for Capital Market Assumptions

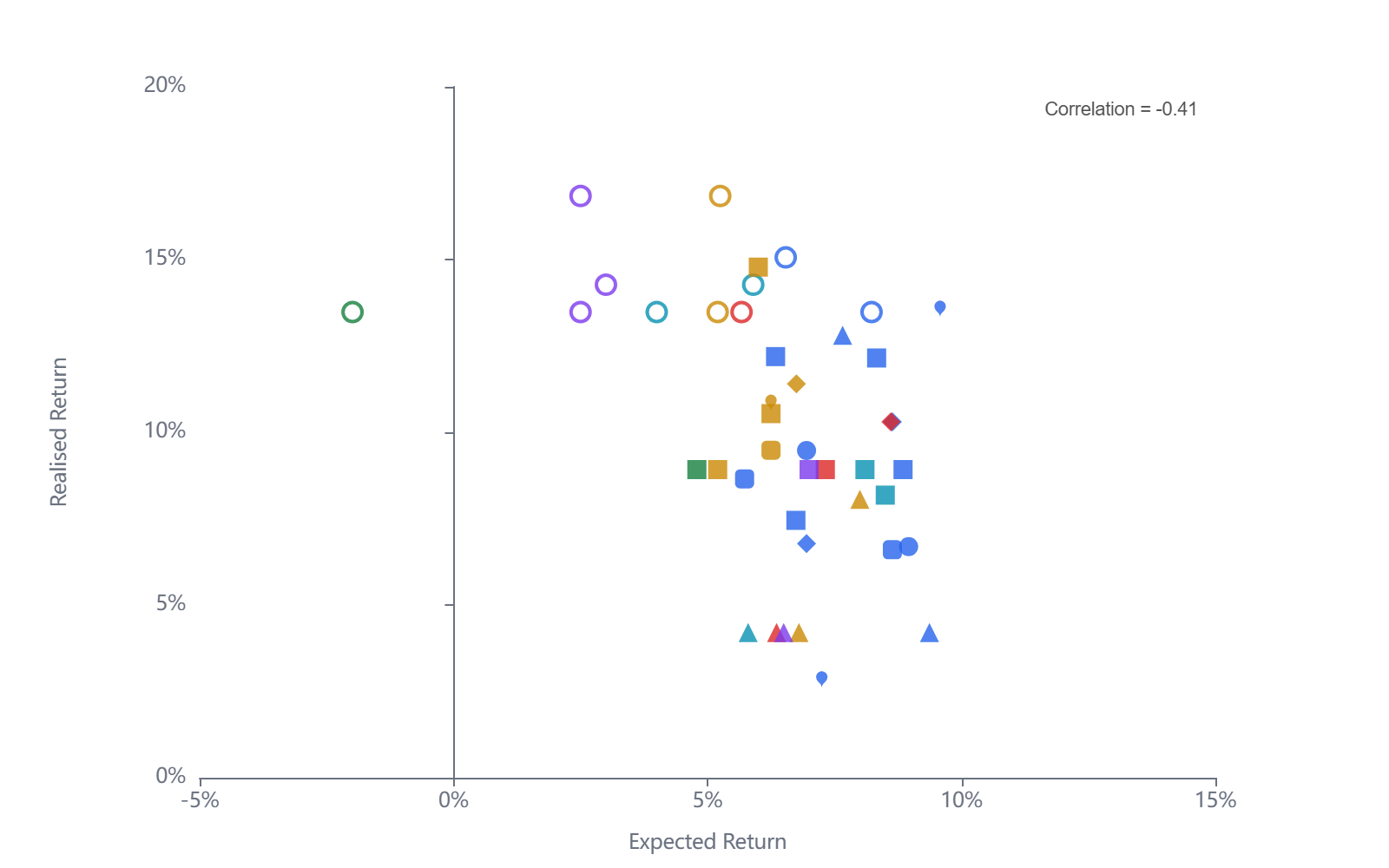

We evaluate the track record of freely available CMAs against subsequently realised returns

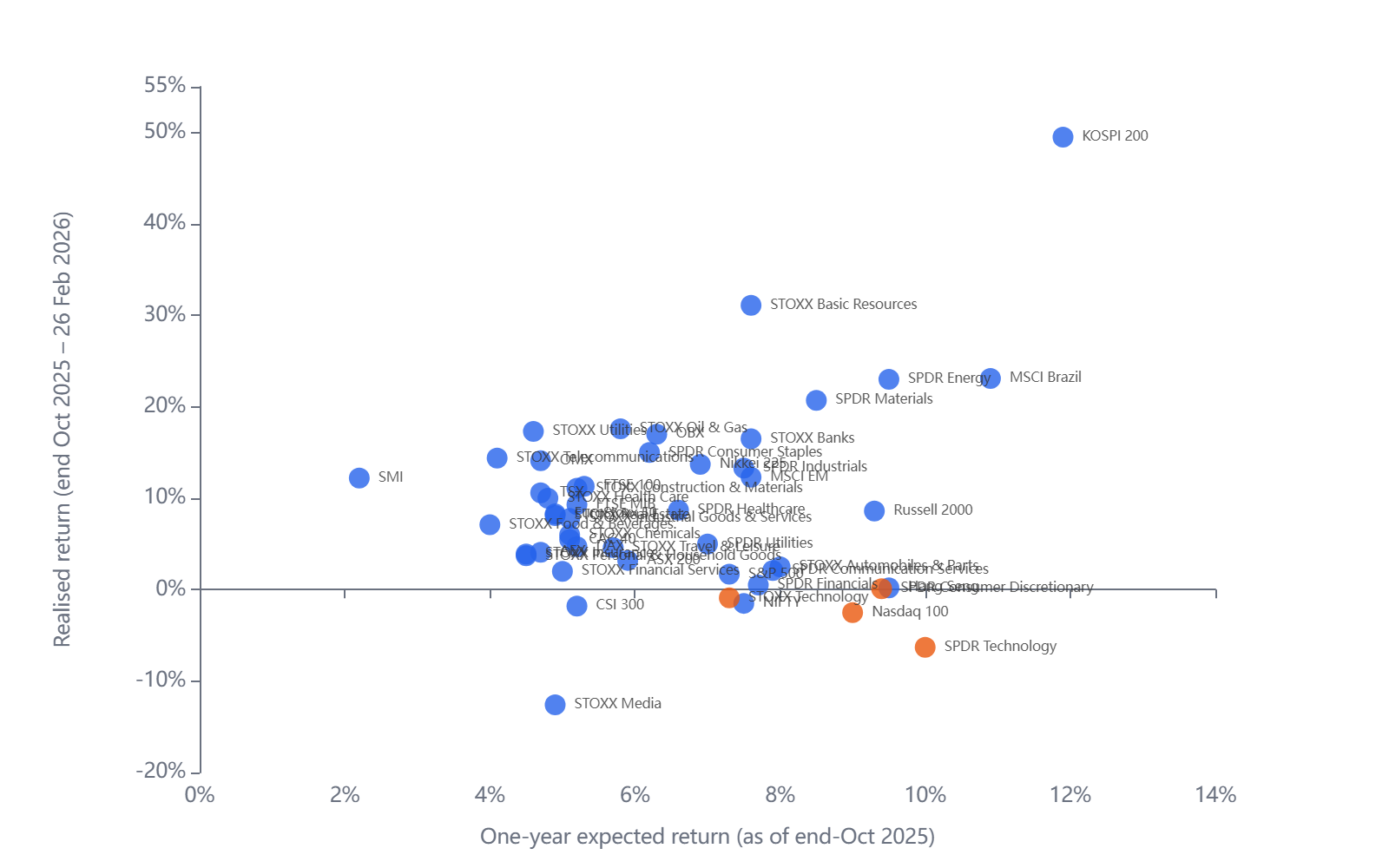

We check in on our expected return estimates from last year and how they compare to realised outcomes.

Why sovereign fund allocation decisions need to account for macro dynamics — not just portfolio returns.

How can institutional investors integrate geopolitical scenario analysis into their asset allocation processes?

We break down the drivers of rising Japanese government bond yields.

Why equity performance didn't match the re-pricing of century bonds.

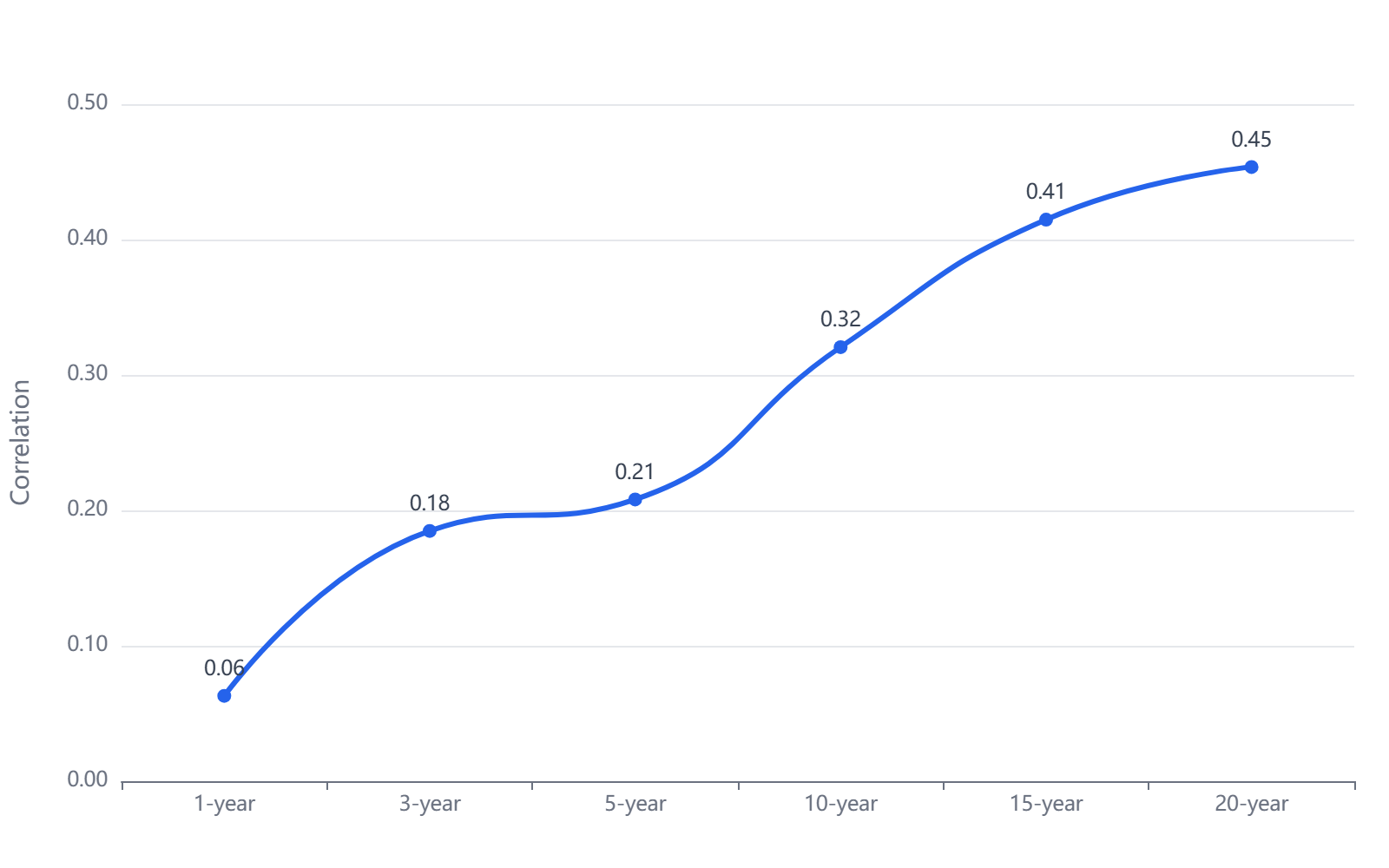

We discuss how correlations change over different investment horizons.